Late yesterday afternoon a judge denied the motion from the National Mortgage Brokers Association to issue a temporary restraining order on the Federal Reserve rule regarding loan officer compensation. This is a historic move that will change the landscape of both mortgage lending and more importantly the cost of borrowing to consumers. To see the ruling:

CLICK HERE

Thursday, March 31, 2011

Wednesday, March 30, 2011

Gerry Letourneau

Gerry is a real estate agent that works with Chris. Listen to what she has to say about her experience with Chris and Cornerstone Mortgage.

Koven Carlson and Tracy Welsh

Koven and Tracy just closed on the purchase of their new home. Listen to what they have to say about their experience with Cornerstone Mortgage.

Monday, March 28, 2011

Pam and Michael Richards

Pam and Michael just closed on the purchase of a new home with Cornerstone Mortgage. Listen to what they have to say about their experience.

Friday, March 25, 2011

Thursday, March 17, 2011

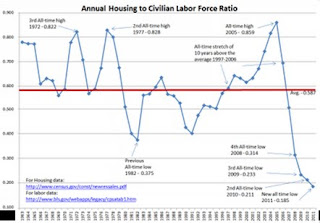

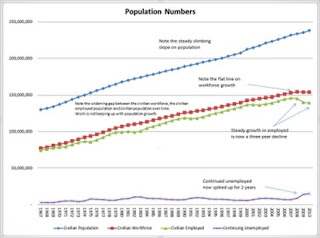

Here is an interesting set of charts on labor pool statistics and housing. First consider a chart of various civilian population numbers.

Civilian Population, Workforce, Employment

The civilian population is steadily rising. However, none of that increase in recent years is looking to buy a home.

Those not in the labor force are not looking

Those unemployed are not looking

Those afraid of losing their job are not looking

Those in a house and underwater are not looking

Those just out of school and deep in school debt are not looking

Those facing retirement may be looking to sell or downsize

Mortgage standards are much tighter for those who are looking

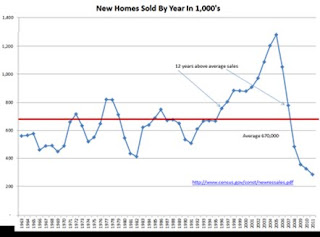

New Home Sales

Here is an interesting set of charts on labor pool statistics and housing. First consider a chart of various civilian population numbers.

Those struggling to understand why home sales are so bad and why they are unlikely to improve much soon, need only consider the previous set of bullet points.

Annualized New Home Sales to Civilian Labor Force Ratio

People do not realize how much of our economy depends on the housing market.

Think of 1,000,000 homes sold in the mid '00's at an average of $290,000 each and you have $290,000,000,000 in GDP.

Today we are down to $200,000 homes and 284,000 of them. That is $56,800,000,000 in GDP, a decrease of $233,200,000,000 plus whatever multiplier, if any, you want to assign to that.

Civilian Population, Workforce, Employment

The civilian population is steadily rising. However, none of that increase in recent years is looking to buy a home.

Those not in the labor force are not looking

Those unemployed are not looking

Those afraid of losing their job are not looking

Those in a house and underwater are not looking

Those just out of school and deep in school debt are not looking

Those facing retirement may be looking to sell or downsize

Mortgage standards are much tighter for those who are looking

New Home Sales

Here is an interesting set of charts on labor pool statistics and housing. First consider a chart of various civilian population numbers.

Those struggling to understand why home sales are so bad and why they are unlikely to improve much soon, need only consider the previous set of bullet points.

Annualized New Home Sales to Civilian Labor Force Ratio

People do not realize how much of our economy depends on the housing market.

Think of 1,000,000 homes sold in the mid '00's at an average of $290,000 each and you have $290,000,000,000 in GDP.

Today we are down to $200,000 homes and 284,000 of them. That is $56,800,000,000 in GDP, a decrease of $233,200,000,000 plus whatever multiplier, if any, you want to assign to that.

Wednesday, March 16, 2011

Economics: US HOUSING STARTS

Tanked in February, to a 479k pace vs 618k in January revised from 596k and a median estimate of 577k. Single family starts fell 11.8% in the month following a 1.4% gain in January, while the more volatile multi family starts series fell 46.1% following a 87.4% gain. Permit issuance fell to 517k vs a prior 563k, suggesting that while the February decline in starts was exaggerated, the trend is downward. Permits for singles fell 9.3%, multis 4.9%. Completions jumped 13.9% in the month, and homes under construction were fairly steady, so while starts will drag down the totals later in Q1, the GDP impact from housing was not bad at the beginning of the quarter. Housing starts in February were the 2nd lowest on record, right behind April of 2009. That result is not all that remarkable, because housing starts had not climbed very far from the record low in any of the intervening months. Starts have been somewhat noisy the past couple of months, but the 3mo average is running at just about the same level now as in December and January, better than back in the low point in 2009 by just a bit. When it comes to permits, though, we have a new record. The 517k permits reported for February is just a tad lower than the prior 522k low posted in March of 2009, the permits that led to the record low level of starts in April 2009. While permits running above starts is a good sign, record low permits is not.

Tuesday, March 15, 2011

For Housing Rebound, Once Again It's Wait Until Next Year

The glimmer of hope that housing would stage a sustainable comeback this spring has melted with the winter snow.

Even as many await the traditional surge of buyers and sellers in the warmer months, analysts say it will be a year before there's any solid improvement in housing.

"We are going to be disappointed the rest of 2011," says Paul Dales, senior US economist at Capital Economics. "There's still weak demand, too many houses on the market. Things won't get better until 2012."

"2011 will be a real challenge, just like 2010," says Bob Walters, chief economist and vice president at QuickenLoans.com. "The key reason is that the jobs picture is still not bright enough. Plus, more foreclosures are coming. Many homes are still 'under water' or worth less than the loans, so it's going to be rough."

What caused a short-term bounce for housing-and talk of a possible turnaround in 2011-were better numbers for building permits, housing starts and existing home sales for the last months of 2010. Existing home sales were up 5.3 percent overall in 2010, according to the National Association of Realtors.

But new home sales and building permits have recently reversed themselves or remain in a downward trend. In fact, new home sales reached a record 47-year low this past year, with an annual decrease of 14 percent, according to the Department of Housing.

And Mortgage applications continue to fall, even as rates hover around the historic lows of 5 percent.

In spite of improving bread and butter conditions-like declining job losses and increased business activity -the housing market is standing still.

"There are too many vacant homes and excess inventory in the system now to create a stronger housing market," says Lawrence Yun, chief economist at the National Association of Realtors.

According to RealtyTrac, there were a record 2.9 million foreclosures in 2010. An estimated 50,000 new foreclosure actions are initiated every week, according to the Center for Responsible Lending.

And some 2.2 million homes are delinquent in mortgage payments and could be additional victims of the foreclosure mess.

"When realtors sit down and talk, foreclosures are on our mind," says Johnny Martinelli, the broker/owner of LevyMart Real Estate Sales and Investments in Norman, Oklahoma. "We are seeing more of them. People are scared."

Adding to the fears of realtors is a lack of confidence among consumers, says Michael Freed, a managing partner and real estate lawyer in the firm Brennan, Manna & Diamond.

"You see people in the malls and restaurants, but when it comes to a big purchase like a home, there's not much confidence," Freed explains. "Add that with the dynamics of tougher lending restrictions and higher down payments, and homes are not going to sell."

The lack of sales pretty much covers all income brackets, adds Freed. "It is a buyer's market if you have the money," he says.

It's money-specifically cash-that's keeping housing from sinking even lower, says Julie Reynolds, a vice president at Move, Inc., an online real estate resource.

Cash buyers and investors have driven 70 percent of the increase in existing home sales seen since last July, while first-time buyers have been responsible for just 6 percent, according to Capital Economics.

"Investors who are cash rich are snapping up affordably priced properties," Reynolds says. "They are critical in areas like California, Arizona and Florida that are having problems with distressed homes."

The cash has a foreign flavor, with international buyers from Western Europe, Asia and the Middle East, adds Reynolds.

Those who still need a loan continue to face tougher lending standards-fallout from the housing crash-and gum up the works, say analysts.

"Banks are a problem with the scrutiny for applications," Johnny Martinelli says. "It's slowing up the process. There are a lot of people who can make payments but can't qualify."

Another wrinkle comes at the end of June. A little known portion of the Dodd-Frank financial reform bill ends the so-called 'teaser rates' that misled buyers into deals that turned sour with higher payments. The change, however, may have negative unintended consequences, say experts.

"Starting in April, loan officers won't be paid by the terms of the loan and will get less money," explains real estate attorney Neil Garfinkel of the New York based law firm AGMB. "That might mean they move around looking for better pay. It could also mean fewer loan officers to handle applications."

"Whenever we get momentum something pushes us back," says Alan Rosenbaum, CEO of GuardHill Financial, a mortgage banking and brokerage firm. "The government [with Dodd-Frank] is telling the industry what it can pay and that makes it more expensive for consumers."

Another effect from the housing collapse-and a possible sea change-is a different mind set about how people live, says Freed.

"Americans aren't looking to move like they used to," Freed contends. "It's not necessarily that we've lost our love of owning a home, but I think people are looking at the market differently because of the crash. They're renting, and focusing on a life style they can afford."

So with all the doom and gloom, what will change in 2012 to make housing any better?

"By next year I think you will see stronger demand," says Dale. "The number of foreclosures should peek this year as they flush through the system. I also think the job situation will improve in 2012."

Also helping the market-a wave of refinancing in the adjustable-rate mortgage area, averting additional foreclosures in some cases. About 20 percent of ARMs holders have taken advantage of lower interest rates to refinance; others have been able to pay them them off completely, according to the Mortgage Bankers Assocation.

"I think we are headed in the right direction for next year on inventory and prices," says Walters.

For all the tumult and uncertainty, one thing hasn't changed about the real estate market. Location is key, and parts of the country are having a better 2011 than 2010.

After taking their house off the market last spring, Maria and Michael Treiber of Morris Township, New Jersey sold their three-bedroom, split-level this February after prices had finally climbed to an acceptable level.

"It was much better for us," says Treiber, a local policeman who plans to rent while looking for another home. "There weren't that many homes on the market this time, so that helped."

Some areas are even seeing an uptick in new construction.

"There's some new construction, and some people are buying homes," Martinelli says of Norman, Okla. "They're downsizing, but at least there's some activity. It's not as bad as it was last year."

Wall Street bonuses are moving some buyers and renters back to the high-end Hamptons section of Long Island, N.Y.

"Fundamentals are improving if not significantly," says Rosenbaum. "People still need to move, whether for a job or bigger home."

And longtime depressed areas are also seeing daylight.

"Areas like Chicago, Detroit, Las Vegas that have a lot of foreclosures are on an upswing with interest in home buying," says Reynolds. "That interest is better than a year ago."

Above all, there's an acceptance of the new normal in housing, says Jim Gillespie, CEO of real estate firm Caldwell Banker.

"Happiness is a new base, but we are going up," Gillespie says. "At the worst, things will stay the same; at best, we'll have a slow recovery. I don't think Americans have lost their love of owning a home. We're just obviously going through a tough time."

Even as many await the traditional surge of buyers and sellers in the warmer months, analysts say it will be a year before there's any solid improvement in housing.

"We are going to be disappointed the rest of 2011," says Paul Dales, senior US economist at Capital Economics. "There's still weak demand, too many houses on the market. Things won't get better until 2012."

"2011 will be a real challenge, just like 2010," says Bob Walters, chief economist and vice president at QuickenLoans.com. "The key reason is that the jobs picture is still not bright enough. Plus, more foreclosures are coming. Many homes are still 'under water' or worth less than the loans, so it's going to be rough."

What caused a short-term bounce for housing-and talk of a possible turnaround in 2011-were better numbers for building permits, housing starts and existing home sales for the last months of 2010. Existing home sales were up 5.3 percent overall in 2010, according to the National Association of Realtors.

But new home sales and building permits have recently reversed themselves or remain in a downward trend. In fact, new home sales reached a record 47-year low this past year, with an annual decrease of 14 percent, according to the Department of Housing.

And Mortgage applications continue to fall, even as rates hover around the historic lows of 5 percent.

In spite of improving bread and butter conditions-like declining job losses and increased business activity -the housing market is standing still.

"There are too many vacant homes and excess inventory in the system now to create a stronger housing market," says Lawrence Yun, chief economist at the National Association of Realtors.

According to RealtyTrac, there were a record 2.9 million foreclosures in 2010. An estimated 50,000 new foreclosure actions are initiated every week, according to the Center for Responsible Lending.

And some 2.2 million homes are delinquent in mortgage payments and could be additional victims of the foreclosure mess.

"When realtors sit down and talk, foreclosures are on our mind," says Johnny Martinelli, the broker/owner of LevyMart Real Estate Sales and Investments in Norman, Oklahoma. "We are seeing more of them. People are scared."

Adding to the fears of realtors is a lack of confidence among consumers, says Michael Freed, a managing partner and real estate lawyer in the firm Brennan, Manna & Diamond.

"You see people in the malls and restaurants, but when it comes to a big purchase like a home, there's not much confidence," Freed explains. "Add that with the dynamics of tougher lending restrictions and higher down payments, and homes are not going to sell."

The lack of sales pretty much covers all income brackets, adds Freed. "It is a buyer's market if you have the money," he says.

It's money-specifically cash-that's keeping housing from sinking even lower, says Julie Reynolds, a vice president at Move, Inc., an online real estate resource.

Cash buyers and investors have driven 70 percent of the increase in existing home sales seen since last July, while first-time buyers have been responsible for just 6 percent, according to Capital Economics.

"Investors who are cash rich are snapping up affordably priced properties," Reynolds says. "They are critical in areas like California, Arizona and Florida that are having problems with distressed homes."

The cash has a foreign flavor, with international buyers from Western Europe, Asia and the Middle East, adds Reynolds.

Those who still need a loan continue to face tougher lending standards-fallout from the housing crash-and gum up the works, say analysts.

"Banks are a problem with the scrutiny for applications," Johnny Martinelli says. "It's slowing up the process. There are a lot of people who can make payments but can't qualify."

Another wrinkle comes at the end of June. A little known portion of the Dodd-Frank financial reform bill ends the so-called 'teaser rates' that misled buyers into deals that turned sour with higher payments. The change, however, may have negative unintended consequences, say experts.

"Starting in April, loan officers won't be paid by the terms of the loan and will get less money," explains real estate attorney Neil Garfinkel of the New York based law firm AGMB. "That might mean they move around looking for better pay. It could also mean fewer loan officers to handle applications."

"Whenever we get momentum something pushes us back," says Alan Rosenbaum, CEO of GuardHill Financial, a mortgage banking and brokerage firm. "The government [with Dodd-Frank] is telling the industry what it can pay and that makes it more expensive for consumers."

Another effect from the housing collapse-and a possible sea change-is a different mind set about how people live, says Freed.

"Americans aren't looking to move like they used to," Freed contends. "It's not necessarily that we've lost our love of owning a home, but I think people are looking at the market differently because of the crash. They're renting, and focusing on a life style they can afford."

So with all the doom and gloom, what will change in 2012 to make housing any better?

"By next year I think you will see stronger demand," says Dale. "The number of foreclosures should peek this year as they flush through the system. I also think the job situation will improve in 2012."

Also helping the market-a wave of refinancing in the adjustable-rate mortgage area, averting additional foreclosures in some cases. About 20 percent of ARMs holders have taken advantage of lower interest rates to refinance; others have been able to pay them them off completely, according to the Mortgage Bankers Assocation.

"I think we are headed in the right direction for next year on inventory and prices," says Walters.

For all the tumult and uncertainty, one thing hasn't changed about the real estate market. Location is key, and parts of the country are having a better 2011 than 2010.

After taking their house off the market last spring, Maria and Michael Treiber of Morris Township, New Jersey sold their three-bedroom, split-level this February after prices had finally climbed to an acceptable level.

"It was much better for us," says Treiber, a local policeman who plans to rent while looking for another home. "There weren't that many homes on the market this time, so that helped."

Some areas are even seeing an uptick in new construction.

"There's some new construction, and some people are buying homes," Martinelli says of Norman, Okla. "They're downsizing, but at least there's some activity. It's not as bad as it was last year."

Wall Street bonuses are moving some buyers and renters back to the high-end Hamptons section of Long Island, N.Y.

"Fundamentals are improving if not significantly," says Rosenbaum. "People still need to move, whether for a job or bigger home."

And longtime depressed areas are also seeing daylight.

"Areas like Chicago, Detroit, Las Vegas that have a lot of foreclosures are on an upswing with interest in home buying," says Reynolds. "That interest is better than a year ago."

Above all, there's an acceptance of the new normal in housing, says Jim Gillespie, CEO of real estate firm Caldwell Banker.

"Happiness is a new base, but we are going up," Gillespie says. "At the worst, things will stay the same; at best, we'll have a slow recovery. I don't think Americans have lost their love of owning a home. We're just obviously going through a tough time."

Monday, March 14, 2011

Economics: Irish Banks Seek to Delay 'Evil Day' as Home-Loan Losses Rise

And you thought things were bad in the USA...

March 11 (Bloomberg) -- Perched on a chair overlooking a wood panel-lined

room in Dublin's High Court, a bespectacled Judge Elizabeth Dunne has become

all-too-used to hearing from the victims of Ireland's economic meltdown.

Each Monday, Dunne presides over repossession hearings, with one in 10

Irish mortgages now in trouble. At the end of last year, more than 79,000

borrowers were behind on payments or had loan terms altered due to

"financial distress," the country's central bank said on Feb. 28.

"Things are getting worse and worse," said Dunne, as she weighed the case

of a couple about 114,000 euros ($158,000) in arrears on a 558,938-euro home

loan, one of 74 cases on her list on March 7. "Putting off the evil day is

not going to help."

Irish mortgages account for more than a third of about 270 billion euros of

loans that remain with the nation's so-called viable lenders -- Allied Irish

Banks Plc, Bank of Ireland Plc, Irish Life & Permanent Plc and EBS Building

Society. The country's new coalition parties are not convinced "that there

has been proper transparency or full disclosure by the banks" on home-loan

impairments, Alan Shatter told RTE Radio on March 7, two days before his

appointment as Minister for Justice.

"There has been a continual under-estimation of loan impairments in Irish

banks over the past few years," Ray Kinsella, banking professor at the

Smurfit Business School at University College Dublin, said by telephone. "I

am seriously concerned about mounting loan losses in their mortgage books."

New Stress Test

The bad loans may be reassessed as early as this month when Ireland's

central bank concludes a third round of stress tests on the country's

lenders. The results will determine how much of a 35 billion-euro

international bailout fund Ireland will need to draw down.

A year ago, Irish regulators stress-tested for a 5 percent loss rate on

Irish mortgages. This year's review "will take account of the deteriorating

economic conditions and hence" loan-loss assumptions "may be higher," said

Nicola Faulkner, a spokeswoman for the central bank, by e-mail.

Ireland is suffering after a decade-long real estate boom collapsed in

2007. Already, the state has bought 72.3 billion euros of risky commercial

property loans from the banks, at an average discount of 58 percent. Irish

house prices, which quadrupled in the decade to 2007, have since plunged

more than a third. Unemployment has tripled to 13.5 percent over the same

period.

House Price Declines

This year's tests may stress loan books against the unemployment rate

rising to 16 percent, house prices falling 60 percent from their peak and

"negligible" economic growth, said analysts including Jim Ryan and Michael

Cummins of Glas Securities, the Dublin-based fixed-income firm, in a note to

clients March 9. The central bank declined to comment.

More than 300,000 households, or about 40 percent of mortgages, may find

their mortgages are worth more than their homes, so-called negative equity,

before the property market bottoms out, said David Duffy, an economist at

the Economic & Social Research Institute in Dublin, who estimates that house

prices will fall by as much as half from peak to trough.

Morgan Kelly, a University College Dublin economics professor dubbed

"Doctor Doom" for his bleak assessments of Ireland's housing market, wrote

in the Irish Times on Nov. 8 that banks face "mass mortgage defaults" and a

"wave of foreclosures." Kelly declined to be interviewed.

EU Bailout

Iceland, where almost 40 percent of residential mortgages were in negative

equity by December, decided that month to write off mortgages and other

household debt by as much as $858 million. Unlike Ireland and other western

nations, the Nordic nation placed its biggest lenders in receivership in

2008 rather than offer taxpayer-funded capital injections.

Ireland has bolstered its banks with 46.3 billion euros of additional

capital over the past two years. The nation was forced to agree to an 85

billion-euro bailout on Nov. 28, led by the European Union and the

International Monetary Fund. That package includes 10 billion euros to

recapitalize the banks up- front and a further 25 billion euros of

"contingency" capital to be used if required.

"When the teams from the EU, ECB and IMF arrived in November, they probably

thought they would find huge holes remaining in the banks' loan books, but

they did not," said Alan Ahearne, who was economics adviser to Brian

Lenihan, the former finance minister. "It's not that there's some black hole

in the Irish banks that hasn't previously been discovered."

10 Billion Euros

Still, a previous regulatory target for banks to hold 8 percent core tier 1

capital, a gauge of financial stability, "wasn't enough to support

confidence in the banks" given the economy's problems, Ahearne said. Ireland

agreed as part of the bailout to increase lenders' capital levels to no less

than 10.5 percent by the end of this month.

The 10 billion euros of initial capital destined for banks under the rescue

package "pretty much covers our base case scenario" for remaining losses in

Irish banks, said Ross Abercromby, a London-based analyst at Moody's

Investors Service, by telephone. "The additional 25 billion euros

contingency fund would cover our stress scenario, which is pretty severe."

Moody's estimates that losses on Irish mortgages may be as high as 14

percent where the loan-to-value ratio is over 90 percent. That rises to 16

percent "in our worst case," the ratings company said.

Household debt soared from 48 percent of disposable income in 1995 to 176

percent in 2009, catapulting Irish consumers into fourth place in 2008 in an

international league table of personal indebtedness from 17th place in 1995,

according to Ireland's Law Reform Commission.

Savings Rise

On the other hand, Irish households' net savings as a percentage of

disposable income rose from zero in 2007 to 12 percent in 2009, according to

the Central Statistics Office. The savings rate should remain around the

same level for this year and next, the ESRI said on Jan. 20.

Irish Life & Permanent Plc Finance Director David McCarthy said he doesn't

believe there are undiscovered losses in banks' mortgage books. The group,

which has 26.3 billion euros of Irish home loans, saw arrears of less than

90 days peak in mid-2010, McCarthy said on March 2, and they've "been

falling, albeit quite slowly, since then," he said.

Bank of Ireland spokeswoman Anne Mathews referred to CEO Richie Boucher's

Nov. 12 statement to analysts that there was "clear evidence" that arrears

were "beginning to stabilize." Allied Irish and EBS spokesmen declined to

comment.

'Different Phenomenon'

The Irish home-loan market is "a totally different phenomenon" to the

commercial real-estate market, said John Reynolds, chief executive officer

of Belgian-owned KBC Ireland.

"Irish banks have been hamstrung by a narrative that has been allowed to

develop that all their lending was as mad as their real-estate lending,"

said Reynolds. "The reality is that the Irish banks, when they didn't do the

real-estate stuff, which was a seductive drug, did bog-standard,

criteria-driven lending."

"Banks are exercising huge forbearance on borrowers in arrears," partly

because of pressure from the authorities "but also because they don't want

to repossess houses as there's no second-hand market to sell them," said

Kinsella, the banking professor. Lenders only held 585 repossessed

residential properties at end-2010, according to the central bank.

The new government said on March 6 it may bring in a two- year moratorium

on repossessions "of modest family homes where a family makes an honest

effort to pay their mortgages." Currently, mortgage holders can enjoy

12-month protection from legal action if they are co-operating with lenders.

The coalition also pledged to fast-track changes in laws requiring

bankrupted individuals to wait 12 years before they are discharged from

their debts.

Rising Interest Rates

The issue of full recourse for mortgage loans is positive for banks, if not

for borrowers in negative equity, said Abercromby. "If that level of

recourse is watered down, by introducing less stringent bankruptcy laws, you

could be looking at higher losses," he said.

There is also concern that rising interest rates will hit borrowers who

have managed to remain out of trouble so far. ECB President Jean-Claude

Trichet signaled on March 3 the bank may raise its benchmark rate from a

record low of 1 percent as soon as next month.

Banks have already increased variable home loan rates from an average of

3.16 percent in mid-2009 to 3.87 percent by November, according to the ESRI.

Lenders, including Irish Life and EBS, have hiked borrowing costs again

since then.

Meanwhile, at least half of all Irish mortgages are so- called tracker

products, with pricing linked to ECB's key rate, according to the Irish

Banking Federation.

Tracker Rates

While banks may be able to contain bad-loan losses on their mortgage books,

"a big and ongoing problem is that a large part of their mortgage books are

based on ECB tracker rates, which banks are funding at a loss," said Karl

Deeter, operations manager with Dublin-based Irish Mortgage Brokers.

Back in the High Court, Dunne is listening to how a house builder from Co.

Cavan, close to the border with Northern Ireland, is 67,000 euros in arrears

on a 360,000 euro home loan taken out three years ago.

Times are hard out there, says the man, who has a plant hire and quarrying

business, but is making partial remortgage payments. "I understand that

well," says Dunne. "I see that every Monday."

March 11 (Bloomberg) -- Perched on a chair overlooking a wood panel-lined

room in Dublin's High Court, a bespectacled Judge Elizabeth Dunne has become

all-too-used to hearing from the victims of Ireland's economic meltdown.

Each Monday, Dunne presides over repossession hearings, with one in 10

Irish mortgages now in trouble. At the end of last year, more than 79,000

borrowers were behind on payments or had loan terms altered due to

"financial distress," the country's central bank said on Feb. 28.

"Things are getting worse and worse," said Dunne, as she weighed the case

of a couple about 114,000 euros ($158,000) in arrears on a 558,938-euro home

loan, one of 74 cases on her list on March 7. "Putting off the evil day is

not going to help."

Irish mortgages account for more than a third of about 270 billion euros of

loans that remain with the nation's so-called viable lenders -- Allied Irish

Banks Plc, Bank of Ireland Plc, Irish Life & Permanent Plc and EBS Building

Society. The country's new coalition parties are not convinced "that there

has been proper transparency or full disclosure by the banks" on home-loan

impairments, Alan Shatter told RTE Radio on March 7, two days before his

appointment as Minister for Justice.

"There has been a continual under-estimation of loan impairments in Irish

banks over the past few years," Ray Kinsella, banking professor at the

Smurfit Business School at University College Dublin, said by telephone. "I

am seriously concerned about mounting loan losses in their mortgage books."

New Stress Test

The bad loans may be reassessed as early as this month when Ireland's

central bank concludes a third round of stress tests on the country's

lenders. The results will determine how much of a 35 billion-euro

international bailout fund Ireland will need to draw down.

A year ago, Irish regulators stress-tested for a 5 percent loss rate on

Irish mortgages. This year's review "will take account of the deteriorating

economic conditions and hence" loan-loss assumptions "may be higher," said

Nicola Faulkner, a spokeswoman for the central bank, by e-mail.

Ireland is suffering after a decade-long real estate boom collapsed in

2007. Already, the state has bought 72.3 billion euros of risky commercial

property loans from the banks, at an average discount of 58 percent. Irish

house prices, which quadrupled in the decade to 2007, have since plunged

more than a third. Unemployment has tripled to 13.5 percent over the same

period.

House Price Declines

This year's tests may stress loan books against the unemployment rate

rising to 16 percent, house prices falling 60 percent from their peak and

"negligible" economic growth, said analysts including Jim Ryan and Michael

Cummins of Glas Securities, the Dublin-based fixed-income firm, in a note to

clients March 9. The central bank declined to comment.

More than 300,000 households, or about 40 percent of mortgages, may find

their mortgages are worth more than their homes, so-called negative equity,

before the property market bottoms out, said David Duffy, an economist at

the Economic & Social Research Institute in Dublin, who estimates that house

prices will fall by as much as half from peak to trough.

Morgan Kelly, a University College Dublin economics professor dubbed

"Doctor Doom" for his bleak assessments of Ireland's housing market, wrote

in the Irish Times on Nov. 8 that banks face "mass mortgage defaults" and a

"wave of foreclosures." Kelly declined to be interviewed.

EU Bailout

Iceland, where almost 40 percent of residential mortgages were in negative

equity by December, decided that month to write off mortgages and other

household debt by as much as $858 million. Unlike Ireland and other western

nations, the Nordic nation placed its biggest lenders in receivership in

2008 rather than offer taxpayer-funded capital injections.

Ireland has bolstered its banks with 46.3 billion euros of additional

capital over the past two years. The nation was forced to agree to an 85

billion-euro bailout on Nov. 28, led by the European Union and the

International Monetary Fund. That package includes 10 billion euros to

recapitalize the banks up- front and a further 25 billion euros of

"contingency" capital to be used if required.

"When the teams from the EU, ECB and IMF arrived in November, they probably

thought they would find huge holes remaining in the banks' loan books, but

they did not," said Alan Ahearne, who was economics adviser to Brian

Lenihan, the former finance minister. "It's not that there's some black hole

in the Irish banks that hasn't previously been discovered."

10 Billion Euros

Still, a previous regulatory target for banks to hold 8 percent core tier 1

capital, a gauge of financial stability, "wasn't enough to support

confidence in the banks" given the economy's problems, Ahearne said. Ireland

agreed as part of the bailout to increase lenders' capital levels to no less

than 10.5 percent by the end of this month.

The 10 billion euros of initial capital destined for banks under the rescue

package "pretty much covers our base case scenario" for remaining losses in

Irish banks, said Ross Abercromby, a London-based analyst at Moody's

Investors Service, by telephone. "The additional 25 billion euros

contingency fund would cover our stress scenario, which is pretty severe."

Moody's estimates that losses on Irish mortgages may be as high as 14

percent where the loan-to-value ratio is over 90 percent. That rises to 16

percent "in our worst case," the ratings company said.

Household debt soared from 48 percent of disposable income in 1995 to 176

percent in 2009, catapulting Irish consumers into fourth place in 2008 in an

international league table of personal indebtedness from 17th place in 1995,

according to Ireland's Law Reform Commission.

Savings Rise

On the other hand, Irish households' net savings as a percentage of

disposable income rose from zero in 2007 to 12 percent in 2009, according to

the Central Statistics Office. The savings rate should remain around the

same level for this year and next, the ESRI said on Jan. 20.

Irish Life & Permanent Plc Finance Director David McCarthy said he doesn't

believe there are undiscovered losses in banks' mortgage books. The group,

which has 26.3 billion euros of Irish home loans, saw arrears of less than

90 days peak in mid-2010, McCarthy said on March 2, and they've "been

falling, albeit quite slowly, since then," he said.

Bank of Ireland spokeswoman Anne Mathews referred to CEO Richie Boucher's

Nov. 12 statement to analysts that there was "clear evidence" that arrears

were "beginning to stabilize." Allied Irish and EBS spokesmen declined to

comment.

'Different Phenomenon'

The Irish home-loan market is "a totally different phenomenon" to the

commercial real-estate market, said John Reynolds, chief executive officer

of Belgian-owned KBC Ireland.

"Irish banks have been hamstrung by a narrative that has been allowed to

develop that all their lending was as mad as their real-estate lending,"

said Reynolds. "The reality is that the Irish banks, when they didn't do the

real-estate stuff, which was a seductive drug, did bog-standard,

criteria-driven lending."

"Banks are exercising huge forbearance on borrowers in arrears," partly

because of pressure from the authorities "but also because they don't want

to repossess houses as there's no second-hand market to sell them," said

Kinsella, the banking professor. Lenders only held 585 repossessed

residential properties at end-2010, according to the central bank.

The new government said on March 6 it may bring in a two- year moratorium

on repossessions "of modest family homes where a family makes an honest

effort to pay their mortgages." Currently, mortgage holders can enjoy

12-month protection from legal action if they are co-operating with lenders.

The coalition also pledged to fast-track changes in laws requiring

bankrupted individuals to wait 12 years before they are discharged from

their debts.

Rising Interest Rates

The issue of full recourse for mortgage loans is positive for banks, if not

for borrowers in negative equity, said Abercromby. "If that level of

recourse is watered down, by introducing less stringent bankruptcy laws, you

could be looking at higher losses," he said.

There is also concern that rising interest rates will hit borrowers who

have managed to remain out of trouble so far. ECB President Jean-Claude

Trichet signaled on March 3 the bank may raise its benchmark rate from a

record low of 1 percent as soon as next month.

Banks have already increased variable home loan rates from an average of

3.16 percent in mid-2009 to 3.87 percent by November, according to the ESRI.

Lenders, including Irish Life and EBS, have hiked borrowing costs again

since then.

Meanwhile, at least half of all Irish mortgages are so- called tracker

products, with pricing linked to ECB's key rate, according to the Irish

Banking Federation.

Tracker Rates

While banks may be able to contain bad-loan losses on their mortgage books,

"a big and ongoing problem is that a large part of their mortgage books are

based on ECB tracker rates, which banks are funding at a loss," said Karl

Deeter, operations manager with Dublin-based Irish Mortgage Brokers.

Back in the High Court, Dunne is listening to how a house builder from Co.

Cavan, close to the border with Northern Ireland, is 67,000 euros in arrears

on a 360,000 euro home loan taken out three years ago.

Times are hard out there, says the man, who has a plant hire and quarrying

business, but is making partial remortgage payments. "I understand that

well," says Dunne. "I see that every Monday."

Thursday, March 10, 2011

Economics: More on Foreclosures

The January Mortgage Monitor Report released by Lender Processing Services Inc. (LPS) showed that while foreclosure starts decreased in the first month of 2011, they still outnumber foreclosure sales by almost three to one. At the same time, repeat foreclosures, loans that had cured in one way or another, but have fallen back into foreclosure, now account for more than 35% of foreclosure starts. As of the end of January, foreclosure inventories stood at nearly eight times historical averages and 25 times January 2011's level of foreclosure sales, with delinquencies more than double historical norms.

January's LPS Mortgage Monitor Report also showed that the foreclosure process continues to drag out as the timelines for foreclosure starts, days in inventory and sales all continue to extend. Serious delinquencies continue to rise as well. Deterioration in the 90-plus days delinquent category increased last month, for the first time since May 2010. The 90+ category has grown overall, with the largest increase in the 12-plus month category as loans were removed from foreclosure. As of Jan. 31, 2011, there are now more than 2.2 million loans 90 days or more delinquent but not yet in foreclosure, with more than 6.9 million loans in some stage of delinquency or foreclosure.

As reported in LPS' First Look release, other key results from LPS' latest Mortgage Monitor report include:

►Total U.S. loan delinquency rate: 8.9 percent

►Total U.S. foreclosure inventory rate: 4.16 percent

►Total U.S. non-current* loan rate: 13.1 percent

►States with most non-current* loans: Florida, Nevada, Mississippi, Georgia, New Jersey

►States with fewest non-current* loans: Montana, Wyoming, Alaska, South Dakota, North Dakota

Note: Non-current totals combine foreclosures and delinquencies as a percent of active loans in that state. Totals based on LPS Applied Analytics' loan-level database of mortgage assets and are extrapolated to represent the industry.

Unemployment is driving the latest wave of foreclosure pain.

One in every 497 homes in the U.S. received a foreclosure notice in January, according to the latest data from RealtyTrac. In an industry that’s been battered by foreclosures since the housing bubble burst, the number may not seem like news, but these foreclosures are different.

Foreclosures today aren’t heavily dominated by investors that walked away from properties when values started to plunge. And they’re not the unfortunate folks who signed up for an adjustable rate mortgage they could no longer afford the first time their payments reset. Today’s foreclosure rates are ambulance chasers tailing the sirens of unemployment.

“You can almost follow county by county unemployment rates and foreclosures,” said Rick Sharga, senior vice president at RealtyTrac. “What’s driving this activity is the economic downturn and unemployment.”

And it doesn’t always take a dramatic drop in employment numbers to push a city into the red zone. “It’s really the direction of the unemployment rate that matters,” said Patrick Newport, U.S. economist with IHS Global Insight. “In some markets, it really doesn’t take much to topple them,” said Sharga.

This trend has wreaked havoc on real estate values in areas once thought to be stable, such as Seattle, where last year home prices plunged by more than twice the drop seen in Las Vegas during 2010, according to Zillow. While foreclosures are higher in Las Vegas, it—like many other red hot spots of the housing bubble—experienced the crash earlier on while the new trend in foreclosures is now spreading a new season of pain to places where the run up was less pronounced.

California, which had an unemployment rate of 12.5% at the end of 2010 according to data from the Bureau of Labor Statistics (significantly above December’s national average of 9.6%), produced seven of the 10 cities with the highest foreclosure rates in the country last month. The state accounted for 25% of all foreclosures in the nation in January.

To turn things around, Sharga says the markets would need both job creation and a return of consumer confidence. In the mean time, RealtyTrac is predicting that more than three million homes will receive notices this year and between 1.2 and 1.3 million of those will be repossessed.

The company is also keeping its eye on delinquency rates. “There are between $200 and $300 billion in adjustable rate mortgages readjusting this year … [to] much higher payments to marginally qualified home buyers who have lost 30%, 40%, or 50% of their home values,” Sharga says. “It could be a real mess.”

January's LPS Mortgage Monitor Report also showed that the foreclosure process continues to drag out as the timelines for foreclosure starts, days in inventory and sales all continue to extend. Serious delinquencies continue to rise as well. Deterioration in the 90-plus days delinquent category increased last month, for the first time since May 2010. The 90+ category has grown overall, with the largest increase in the 12-plus month category as loans were removed from foreclosure. As of Jan. 31, 2011, there are now more than 2.2 million loans 90 days or more delinquent but not yet in foreclosure, with more than 6.9 million loans in some stage of delinquency or foreclosure.

As reported in LPS' First Look release, other key results from LPS' latest Mortgage Monitor report include:

►Total U.S. loan delinquency rate: 8.9 percent

►Total U.S. foreclosure inventory rate: 4.16 percent

►Total U.S. non-current* loan rate: 13.1 percent

►States with most non-current* loans: Florida, Nevada, Mississippi, Georgia, New Jersey

►States with fewest non-current* loans: Montana, Wyoming, Alaska, South Dakota, North Dakota

Note: Non-current totals combine foreclosures and delinquencies as a percent of active loans in that state. Totals based on LPS Applied Analytics' loan-level database of mortgage assets and are extrapolated to represent the industry.

Unemployment is driving the latest wave of foreclosure pain.

One in every 497 homes in the U.S. received a foreclosure notice in January, according to the latest data from RealtyTrac. In an industry that’s been battered by foreclosures since the housing bubble burst, the number may not seem like news, but these foreclosures are different.

Foreclosures today aren’t heavily dominated by investors that walked away from properties when values started to plunge. And they’re not the unfortunate folks who signed up for an adjustable rate mortgage they could no longer afford the first time their payments reset. Today’s foreclosure rates are ambulance chasers tailing the sirens of unemployment.

“You can almost follow county by county unemployment rates and foreclosures,” said Rick Sharga, senior vice president at RealtyTrac. “What’s driving this activity is the economic downturn and unemployment.”

And it doesn’t always take a dramatic drop in employment numbers to push a city into the red zone. “It’s really the direction of the unemployment rate that matters,” said Patrick Newport, U.S. economist with IHS Global Insight. “In some markets, it really doesn’t take much to topple them,” said Sharga.

This trend has wreaked havoc on real estate values in areas once thought to be stable, such as Seattle, where last year home prices plunged by more than twice the drop seen in Las Vegas during 2010, according to Zillow. While foreclosures are higher in Las Vegas, it—like many other red hot spots of the housing bubble—experienced the crash earlier on while the new trend in foreclosures is now spreading a new season of pain to places where the run up was less pronounced.

California, which had an unemployment rate of 12.5% at the end of 2010 according to data from the Bureau of Labor Statistics (significantly above December’s national average of 9.6%), produced seven of the 10 cities with the highest foreclosure rates in the country last month. The state accounted for 25% of all foreclosures in the nation in January.

To turn things around, Sharga says the markets would need both job creation and a return of consumer confidence. In the mean time, RealtyTrac is predicting that more than three million homes will receive notices this year and between 1.2 and 1.3 million of those will be repossessed.

The company is also keeping its eye on delinquency rates. “There are between $200 and $300 billion in adjustable rate mortgages readjusting this year … [to] much higher payments to marginally qualified home buyers who have lost 30%, 40%, or 50% of their home values,” Sharga says. “It could be a real mess.”

Thursday, March 3, 2011

Economics: Regulators Push 20% Down Payments on Homes

Banking regulators are pushing for mortgage-lending rules that require homeowners to make minimum 20% down payments on loans classified as lower-risk, according to people familiar with the matter.

The proposal is being floated as a way to rewrite the rules for mortgage lending to prevent a rerun of the housing bubble and financial crisis that resulted from years of easy credit. The Dodd-Frank financial overhaul law enacted last year enabled regulators to define a so-called gold-standard residential mortgage that would be exempt from costly new rules.

At least three agencies—the Federal Reserve, the Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency—back a proposal to require home buyers to put down at least 20% of the sales price in order to obtain one of these "qualified residential mortgages." One proposal would also require borrowers to maintain a 75% loan-to-value ratio for refinances, and a 70% loan-to-value for cash-out refinances in which the borrower refinances into a larger loan, according to people familiar with the matter.

Mortgage-finance giants Fannie Mae and Freddie Mac would also be exempt from the rules while they remain in conservatorship, according to these people. The U.S. took over the firms in 2008, and the Obama administration has proposed eventually winding them down.

The behind-the-scenes debate over the proposal could have far-reaching implications for how Americans finance loans, because it addresses how much equity new borrowers should have in their homes.

It is unclear whether the proposal will garner support among other regulators and be acceptable to the White House and Congress. Altogether, six federal agencies—the three supporting the proposal plus the Department of Housing and Urban Development, the Federal Housing Finance Agency and the Securities and Exchange Commission—must sign off on the proposal before it is released for public comment. It could not be determined Tuesday whether all the agencies would support the 20% down-payment standard.

At a congressional hearing Tuesday, HUD Secretary Shaun Donovan said no deal has been reached yet, and that any plan could instead spell out options.

At a separate hearing Tuesday, Treasury Secretary Timothy Geithner said, "We've got to be careful that we get it right." He added, "I'm not sure how much longer it's going to take, but it's going to take a bit longer than we initially expected."

Meanwhile, some lawmakers expressed concerns that the new rules might make it too hard for homeowners to qualify for less risky, and less costly, loans.

Sen. Kay Hagan (D., N.C.) told Federal Reserve Chairman Ben Bernanke that several lawmakers "are really concerned about not making it so restrictive that we can't have as many well-qualified loans as possible."

The proposal was crafted in response to a provision in Dodd-Frank that aimed to improve mortgage-lending standards. Loans that don't meet the standards for "qualified residential mortgages" and are sold to investors as securities will be subject to a "risk retention" rule, which could raise borrowing costs for homeowners.

The risk-retention rule requires banks to keep 5% of the value of all mortgages they securitize on their books. During the housing boom, many lenders passed on all of their mortgages, and all of the risk, to investors. It was designed to force lenders to have "skin in the game" when selling groups ofmortgages packaged as securities.

Critics of the risk-retention rule said it could raise costs for traditionally safer lending products such as long-term, fixed-rate loans with full income documentation. A coalition of consumer advocacy groups and the real-estate industry have warned that defining the rule too narrowly could raise borrowing costs for millions of creditworthy borrowers.

Regulators must issue a rule defining "qualified residential mortgages" by April, and had initially planned to publish a draft proposal late last year. But the process has been delayed by a disagreement about whether to include in the rule national standards for loan servicers, such as how to modify loans for troubled borrowers. The new proposal reflects a compromise among the regulators to include some standards for how and when banks modify loans.

The proposal is being floated as a way to rewrite the rules for mortgage lending to prevent a rerun of the housing bubble and financial crisis that resulted from years of easy credit. The Dodd-Frank financial overhaul law enacted last year enabled regulators to define a so-called gold-standard residential mortgage that would be exempt from costly new rules.

At least three agencies—the Federal Reserve, the Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency—back a proposal to require home buyers to put down at least 20% of the sales price in order to obtain one of these "qualified residential mortgages." One proposal would also require borrowers to maintain a 75% loan-to-value ratio for refinances, and a 70% loan-to-value for cash-out refinances in which the borrower refinances into a larger loan, according to people familiar with the matter.

Mortgage-finance giants Fannie Mae and Freddie Mac would also be exempt from the rules while they remain in conservatorship, according to these people. The U.S. took over the firms in 2008, and the Obama administration has proposed eventually winding them down.

The behind-the-scenes debate over the proposal could have far-reaching implications for how Americans finance loans, because it addresses how much equity new borrowers should have in their homes.

It is unclear whether the proposal will garner support among other regulators and be acceptable to the White House and Congress. Altogether, six federal agencies—the three supporting the proposal plus the Department of Housing and Urban Development, the Federal Housing Finance Agency and the Securities and Exchange Commission—must sign off on the proposal before it is released for public comment. It could not be determined Tuesday whether all the agencies would support the 20% down-payment standard.

At a congressional hearing Tuesday, HUD Secretary Shaun Donovan said no deal has been reached yet, and that any plan could instead spell out options.

At a separate hearing Tuesday, Treasury Secretary Timothy Geithner said, "We've got to be careful that we get it right." He added, "I'm not sure how much longer it's going to take, but it's going to take a bit longer than we initially expected."

Meanwhile, some lawmakers expressed concerns that the new rules might make it too hard for homeowners to qualify for less risky, and less costly, loans.

Sen. Kay Hagan (D., N.C.) told Federal Reserve Chairman Ben Bernanke that several lawmakers "are really concerned about not making it so restrictive that we can't have as many well-qualified loans as possible."

The proposal was crafted in response to a provision in Dodd-Frank that aimed to improve mortgage-lending standards. Loans that don't meet the standards for "qualified residential mortgages" and are sold to investors as securities will be subject to a "risk retention" rule, which could raise borrowing costs for homeowners.

The risk-retention rule requires banks to keep 5% of the value of all mortgages they securitize on their books. During the housing boom, many lenders passed on all of their mortgages, and all of the risk, to investors. It was designed to force lenders to have "skin in the game" when selling groups ofmortgages packaged as securities.

Critics of the risk-retention rule said it could raise costs for traditionally safer lending products such as long-term, fixed-rate loans with full income documentation. A coalition of consumer advocacy groups and the real-estate industry have warned that defining the rule too narrowly could raise borrowing costs for millions of creditworthy borrowers.

Regulators must issue a rule defining "qualified residential mortgages" by April, and had initially planned to publish a draft proposal late last year. But the process has been delayed by a disagreement about whether to include in the rule national standards for loan servicers, such as how to modify loans for troubled borrowers. The new proposal reflects a compromise among the regulators to include some standards for how and when banks modify loans.

Subscribe to:

Posts (Atom)